How the Secure Act Will Help Secure Women's Wealth in Retirement

2 min read

Related Topics

Last month, we reflected on how much work we still must do as a nation to ensure that women can thrive and age with dignity.

A recent survey of adults aged 50+ that NCOA conducted on behalf of Nationwide showed that health care costs—especially long-term care costs—are an overwhelming concern for women.

On average, women’s life expectancy has increased 25 years in the last 100 years. With women living longer, they need more resources in retirement.

Why we need to help women save for retirement

According to our research, more than half of women preparing for retirement want information on how to continue working in retirement. We view the opportunity to work as key to having a good life.

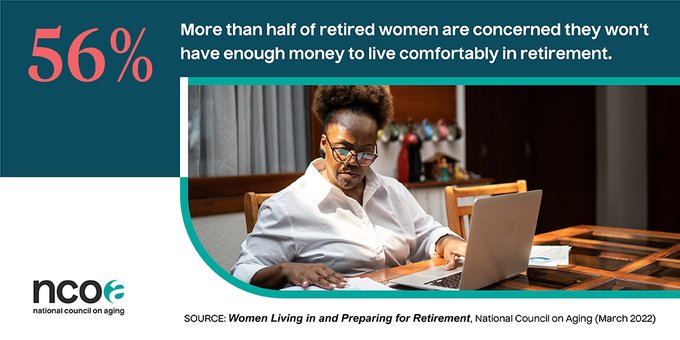

Saving for retirement is also critical. Even though half of the women we surveyed want help setting financial priorities and goals, a third is concerned about finding a source of financial information they can trust. We encourage women to talk to financial professionals about their goals because that’s the only way to see if their values and priorities are aligned.

How the Secure Act 2.0 will positively impact retirement prospects for women

We are delighted that the House of Representatives passed the Secure Act 2.0 with overwhelming bipartisan support on March 29. The act expands employee access to retirement savings plans and makes it easier for employers to enroll employees in these plans. We believe this will go a long way toward offering this tax-advantaged tool that higher-income workers already have. Now the Senate needs to do its part and pass this bill.

There's still more work to be done to help alleviate the strain on women's finances

Congress also must address our caregiving crisis, which impacts women’s retirement prospects, as well. Separate research done by Nationwide shows that Black women who are caregivers spend an average of 34 hours per week caregiving, and they spend an average of $613 per month on caregiving expenses.

That’s a tremendous amount of time and money for a group that has fewer resources to begin with. Not surprisingly, 70% of the women NCOA surveyed said caregiving is a strain on their finances, and 26% said they must postpone retirement because of it.

We are still hoping that the $150 billion for home and community-based services that was included in the Build Back Better Act will be added to Medicaid, which will help low-income women and particularly Black women.

We invite you to dive deeper into our report on Women Living in and Preparing for Retirement.